Exciting news for buyers and sellers alike! On September 18th, the Federal Reserve (the Fed) made a major move, cutting interest rates for the first time in four years. The 50 basis point (0.5%) rate cut is a clear signal of the Fed’s confidence in stabilizing inflation while keeping jobless rates in check. This decision could mark the beginning of a broader rate-cutting cycle, which may last into 2025. The Fed has hinted at an additional 50 basis point cut by year’s end, with the possibility of up to 100 basis points by 2025. However, Fed Chair Jerome Powell urges caution, stating:

“I think we’re going to go carefully meeting by meeting, and make our decisions as we go.”

So, how will these cuts ripple through the housing market, and what does this mean for you as a buyer or seller?

Why a Federal Funds Rate Cut Matters

While the Fed doesn’t set mortgage rates directly, its actions significantly influence them. The Federal Funds Rate impacts the overall economy, including mortgage rates, by affecting borrowing costs for banks. When the Fed cuts rates, it signals easing financial conditions, which typically leads to lower mortgage rates over time. As Mike Fratantoni, Chief Economist at the Mortgage Bankers Association (MBA), says,

“Once the Fed kicks off a rate-cutting cycle, we do expect that mortgage rates will move somewhat lower.”

However, this doesn’t happen overnight; mortgage rates react gradually to Fed rate cuts, making the overall trajectory more important than any single rate cut. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), also highlights that this likely won’t be a one-off rate cut:

“Generally, the rate-cutting cycle is not one-and-done. Six to eight rounds of rate cuts all through 2025 look likely.”

The Projected Impact on Mortgage Rates

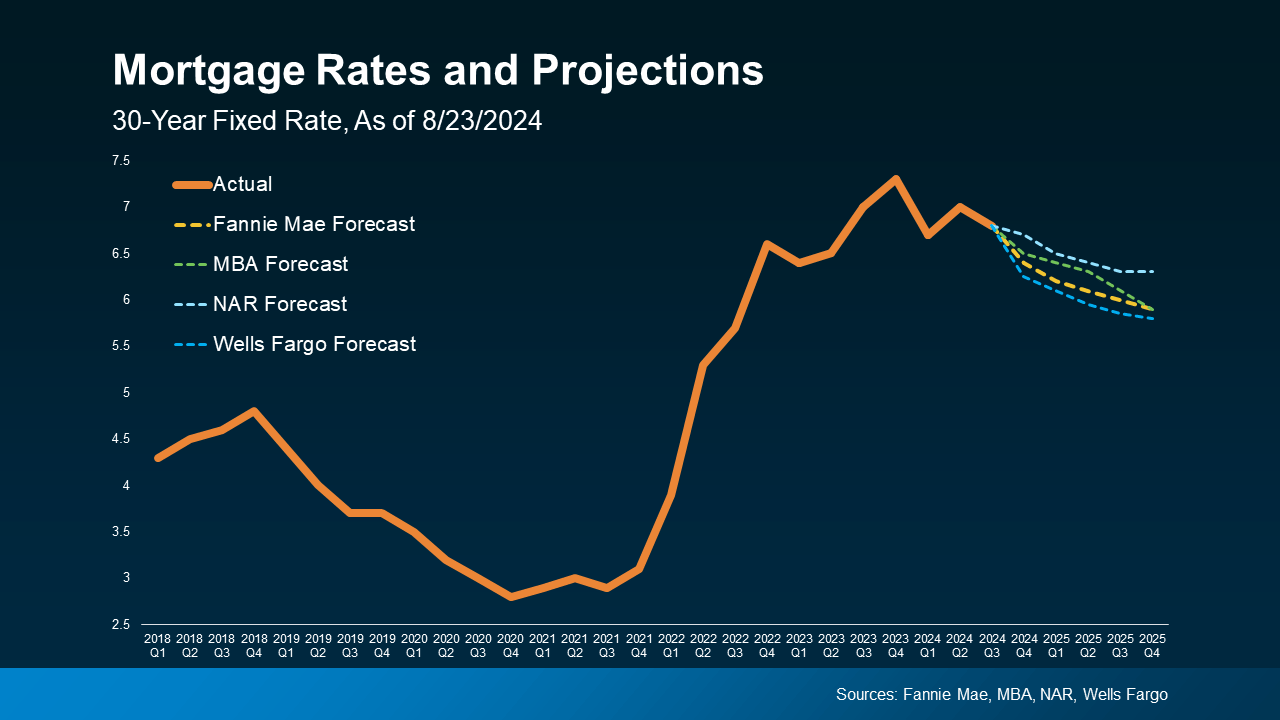

So, what does all this mean for mortgage rates? Experts predict a gradual decline through 2025, driven by the anticipated rate cuts. The graph below shows the most recent forecasts from Fannie Mae, MBA, NAR, and Wells Fargo showing that mortgage rates will likely trend downward (shown in the dotted lines) as the Fed continues to reduce its benchmark interest rate.

Here are two major reasons this is good news for both buyers and sellers:

1. It Helps Alleviate the Lock-In Effect

One of the primary challenges facing the housing market today is the “lock-in effect,” where homeowners are reluctant to sell because they don’t want to lose their existing low-interest mortgage. Many homeowners secured mortgages with rates well below today’s levels during the height of the pandemic when interest rates were historically low.

The prospect of slightly lower mortgage rates could alleviate this effect to some extent. While many sellers may still hesitate to give up their low-rate mortgages, even a modest reduction in rates might encourage some to enter the market. As rates dip, homeowners who have been on the fence might finally feel that upgrading to a new home or relocating is financially feasible again.

However, it’s unlikely that lower rates alone will cause a flood of new listings. The psychological hurdle of giving up a 3% or 4% mortgage for something around 6% is still significant, even if it’s lower than current levels.

2. It Should Boost Buyer Activity

For potential homebuyers, any reduction in mortgage rates could be a game-changer, boosting buyer activity. Lower rates decrease the overall cost of financing a home, making homeownership more affordable. If mortgage rates fall, buyers who were previously priced out may find that homeownership becomes more attainable.

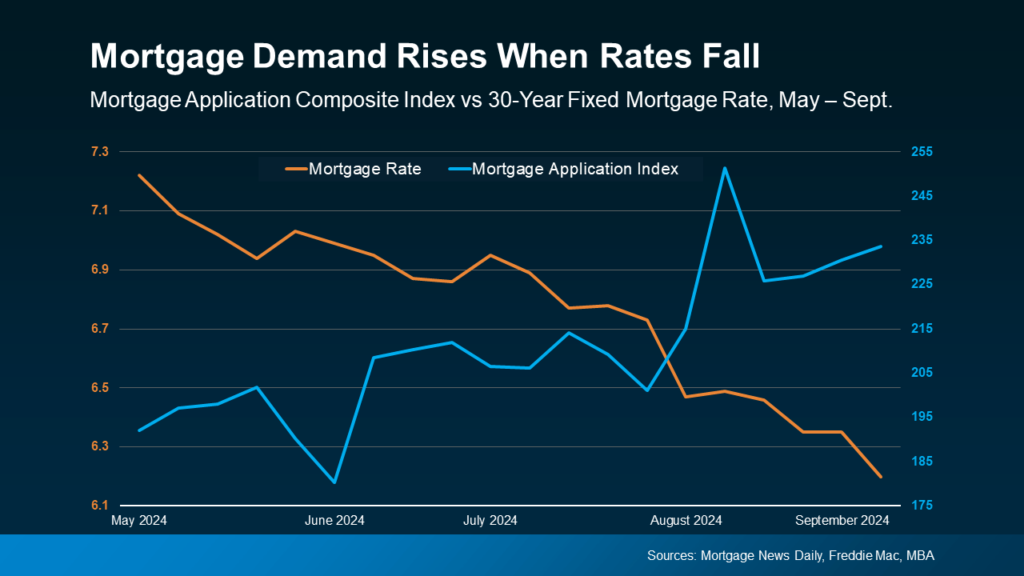

The graph below shows how falling mortgage rates (orange line) lead to increased buyer activity, as indicated by the rise in the MBA Mortgage Application Index (blue line), which tracks mortgage applications. As rates drop, more buyers re-enter the market.

However, this increased demand could come with its own set of challenges. As more buyers jump into the market, there’s a chance that demand will outpace supply, which could drive home prices higher, even as mortgage rates fall. This means that while your monthly payments might be lower due to reduced rates, you could still face higher upfront costs if home prices rise.

What Should You Do?

The Federal Reserve’s rate cuts are set to have a gradual but meaningful impact on the housing market. While mortgage rates won’t drop overnight, they are likely to decline slowly throughout 2024 and 2025. This presents both opportunities and challenges for buyers and sellers alike.

Instead of waiting for perfect conditions, focus on factors you can control, like your financial readiness, and stay informed about the evolving economic landscape. Jacob Channel, Senior Economist at LendingTree, advises:

“Timing the market is basically impossible. If you’re always waiting for perfect market conditions, you’re going to be waiting forever. Buy now only if it’s a good idea for you.”

The takeaway? Don’t wait for mortgage rates to hit rock bottom. If buying aligns with your financial goals, consider acting now, as rates are expected to drop but not return to 2021 lows. As always, I’m here to help guide you through the process so that you make the best decision for your unique situation.